When people think of Nevada, images of bustling casinos and the bright lights of Las Vegas often come to mind. But for families focused on protecting and growing their wealth, Nevada offers something far more valuable: the best trust and estate planning laws in the country.

Nevada has deliberately positioned itself as one of the most trust-friendly jurisdictions in the United States — providing a powerful alternative to offshore structures and offering exceptional benefits for high-net-worth families nationwide. By observing what states like Delaware and South Dakota were doing, Nevada made a conscious decision to become the gold standard for wealth protection and transfer planning.

Here are five major reasons families are moving their trusts — and their financial legacy — to Nevada:

Nevada’s tax environment is one of the most favorable in the country for wealth accumulation. The state has no personal income tax, no estate tax, and no inheritance tax. For families focused on preserving wealth across multiple generations, this can translate into millions of dollars in tax savings over time.

Nevada is a national leader in asset protection. Its laws allow for self-settled spendthrift trusts, often referred to as Nevada Asset Protection Trusts, which shield assets from most future creditors.

Clients often establish Nevada asset protection trusts to safeguard against unforeseen risks such as lawsuits, business disputes, or personal liabilities — all while maintaining control and access under specific conditions.

Nevada’s decanting laws are among the most progressive in the country, allowing families to transfer assets from outdated or inflexible trusts into new trusts with more favorable terms.

Decanting is particularly powerful for families who want to adapt their estate plans to modern laws without needing court intervention — saving time, money, and preserving privacy.

Nevada’s directed trust statutes allow families to divide responsibilities among different advisors — such as investment managers, distribution advisors, and administrative trustees. This gives families more control without sacrificing the protections and oversight of an independent trustee.

For example, a family with LLCs or closely held businesses may want an advisor in their sphere of influence making investment decisions while IconTrust handles the trust administration.

Nevada allows for dynasty trusts — trusts that can last up to 365 years. Compared to states where trust lifespans are severely limited, Nevada offers families the opportunity to create lasting legacies.

Many high-net-worth families create Nevada dynasty trusts to pass down wealth free of state income taxes and federal estate taxes for generations to come.

No matter where you call home, Nevada’s wealth-friendly laws offer powerful tools for securing and growing your family's legacy. Whether your goals involve tax savings, asset protection, or multigenerational planning, partnering with an experienced Nevada trustee can make all the difference.

Interested in learning how a Nevada trust strategy could benefit your family? Contact IconTrust today to start the conversation 702-998-3700.

On July 10, 2023, California Governor Gavin Newsom closed an income tax strategy known as the Nevada incomplete gift non-grantor trust (NING). The law is retroactive to January 1, 2023, and California will now tax any income earned in a NING as if it were a grantor trust, subject to California state income tax. New York banned NING Trusts in 2014, and California has followed suit.

The NING strategy typically involved a California grantor transferring an asset or liquid investments to an incomplete gift non-grantor trust with a Nevada trustee. The transfer must be structured as an incomplete gift for estate tax purposes, and as a non-grantor trust for income tax purposes. These two fact patterns effectively shift the income tax liability to the trust, and since the NING is sitused in Nevada with a Nevada trustee (assuming no other nexus to California) the NING was used to save California state income taxes.

Fortunately, the estate planning industry is usually forward-thinking. Estate planners for California clients can shift from incomplete gift non-grantor trusts to completed gift non-grantor trusts. Many attorneys have been drafting variations of completed gift non-grantor trusts with different themes and variations for California residents for many years out of fear that California would eventually ban the NING strategy. These same strategies have been employed successfully for New York clients since 2014.

The big difference is an incomplete gift is included in your estate at death and will receive a step up in basis. With a completed gift, the assets are outside your estate and will not receive a step up in basis at death. Further, there are federal limitations on the amount that may be gifted to a completed gift non-grantor trust without gift tax.

The current estate tax exemption of $25.84M per married couple (in 2023) should compel California clients to meet with their estate planning attorney as soon as possible before the gift and estate tax exemptions sunset on Jan 1, 2026.

A good breakdown of alternative completed gift non-grantor trusts can be found here: https://ultimateestateplanner.com/2021/04/28/saving-state-income-taxes-ning-trusts-and-completed-gift-non-grantor-options/.

If you have a NING trust, we recommend you contact your estate planning attorney to see how this new legislation will affect your trust and if any changes are necessary.

If you have any questions, please email info@icontrustnv.com.

An effective directed trust is a trust that looks like a traditional trust where the corporate trustee has full powers on paper but operates much like a directed trust.

The difference is in the structure of the assets. In an effective directed trust, the trust owns an LLC membership interest where the corporate trustee is NOT the Manager or Managing Member. Since the trust assets are wrapped in the LLC, which is controlled by the Manager or Managing Member, you have effectively taken the investment discretion away from the corporate trustee.

While there are many benefits of a trust owning an LLC for asset protection, having a trust own an LLC also allows greater flexibility from an investment standpoint. It allows the Manager or Managing Member to buy and sell investments, or oversee a business owned by the LLC, without requiring the corporate trustee to review, sign, and approve such actions. This is especially important when time is of the essence and decisions need to be made quickly.

An effective directed trust is the closest to a client being able to manage their investments as if the trust did not exist. You can make an argument that an effective directed trust is even more seamless than a directed trust. Financial institutions may require the trustee’s involvement for a directed trust because of a lack of understanding of how they operate. However, financial institutions understand LLCs and typically require little to no involvement from the corporate trustee.

Trustees will typically charge based on their liability for the underlying investments in the trust. A directed trust removes the corporate trustee from investment responsibility and liability. Therefore, a trustee’s fee for a directed trust is typically much less. In an effective directed trust, even though the trustee has investment responsibility on paper, you have effectively taken it away by wrapping the assets in an LLC. This is the reason why trustees should charge the same for an effective directed trust as they do for a truly directed trust.

One issue that may preclude an effective directed trust is if the client has a non-grantor trust and the Manager is in a state with a state income tax. If the Manager lives in a state such as California, there is the potential that California will try and tax the income. In this scenario, it might be best to simply name an investment trustee that resides outside of California and have a truly directed trust. We always recommend consulting with a CPA to determine which trust structure makes sense in your estate plan.

Click the button below to download the PDF version:

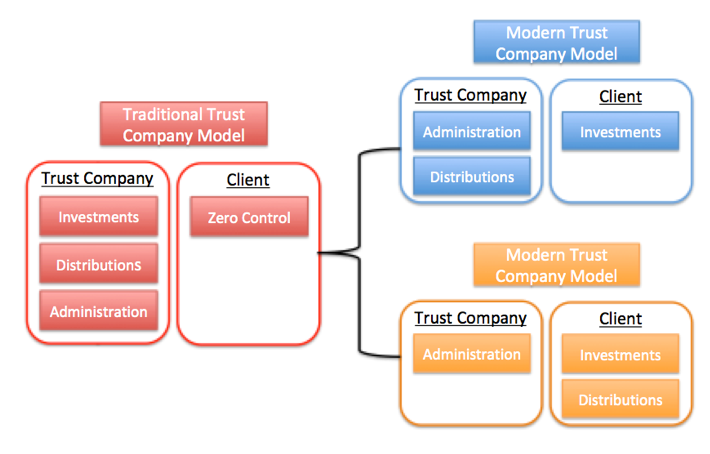

To really understand the benefits of directed trusts, you must first understand the differences between a traditional "delegated" trust and a more modern "directed" trust.

In a traditional trust arrangement, a corporate trustee is responsible for making decisions on investments, distributions, and for the administration of trust assets. All three functions are typically handled in-house. We call this the bundled approach. A trust company may either offer investment management services or delegate investment management to a third party. The trustee still has the ultimate fiduciary responsibility to monitor and oversee the investments and typically will charge a fee based on the market value of the underlying assets, subject to fluctuations in the stock market.

In a directed trust arrangement, the trust document allows for the splitting of trustee duties into multiple roles: an Investment Trustee with the sole discretion to make investment decisions on behalf of the trust, a Distribution Trustee with powers to make or authorize distributions from the trust, and an Administrative Trustee responsible for maintaining books and records and signing tax returns and other documents in an administrative capacity. We call this the unbundled approach. Clients see the value of a corporate trustee for situs, tax, and administration but would prefer to work with their existing professional team of advisors for the investments and perhaps the distribution functions of their trust. A directed trust gives trust grantors, beneficiaries, and their professional advisors more control over a client’s estate plan. Once a cutting-edge planning technique, directed trusts are now the preferred trust structure of the wealthy.

In a directed trust arrangement, the investment management responsibility is removed from the corporate trustee, thus removing the investment liability. This is important because a trustee’s liability for the underlying investments is typically a major factor in determining trustee fees. If the corporate trustee has no investment liability then its fee should be less. Many directed trustees charge a flat fee instead of an asset-based fee to administer a directed trust because of this reduced overall liability.

Given the option, most clients would like to determine what their trust can buy, sell, and hold. They want an advisor they know and trust to manage their investments. They see the value in a corporate trustee administering their trust, but they want the expertise of their trusted financial professionals along the way. Wealthy clients also have nontraditional assets such as, closely-held businesses, family limited partnerships, LLCs, private equity interests, etc., which may not fit under a corporate trustee’s investment parameters. A directed trust allows clients to preserve, protect, and grow these unique assets that are core components to their family’s financial success.

“The task is not to control the wind, but to direct the movements of the ship so that it stays on course.”

Wealthy clients are used to controlling their destiny. They are the captain of their ship, and they like it that way. In estate planning, clients must be willing to give up some level of control, but to the extent they can retain as much as possible, they would prefer it that way. We have discussed giving the client or their trusted financial professional investment discretion in their trust, but some clients also want to give a family member or committee the power to authorize distributions from the trust. They feel this would give more peace of mind and protection for their beneficiaries with fewer restrictions. In a directed trust, they can do just that. The distribution trustee or distribution committee will be able to direct the corporate trustee on when to make a distribution from the trust to a beneficiary.

Nevada has one of the most powerful directed trust statutes in the country. NRS 163.

If you have any questions about directed trusts, please email info@icontrustnv.com or call 702-998-3700.

Are you working with a directed trustee and have been given investment discretion within a trust document? This guide breaks down the three simple options of how the lines of communication work between you, ICON, and a financial advisor.

You have a conversation with your financial advisor about your desire to buy 50 shares of Apple stock.

You call or email ICON directing us to purchase 50 shares of Apple stock.

ICON calls or emails your financial advisor telling them to purchase 50 shares of Apple stock.

A financial advisor has a call with you about the parameters of a fully discretionary investment account. The financial advisor explains that if he/she stays within these parameters the three parties do not have to communicate back and forth.

You confirm with ICON you want to give your financial advisor discretionary approval.

You direct ICON to sign the financial advisor’s discretionary authorization form and Investment Policy Statement (IPS).

ICON calls or emails your financial advisor with confirmation to implement their Investment Policy Statement (IPS).

This is a true bifurcated trust. You have full investment responsibility and should be able to make all investment decisions and direct your financial advisor without any consultation with or involvement by ICON.

*This is how technically it should work, but most of the financial industry/custodians as a whole have not adopted this approach yet.

This guide was created to help you in working with a directed trustee. The goal was to show it is not complicated. The first couple of interactions will be a learning process and once you get the process down, it will be smooth sailing.

Do not hesitate to call your trust officer if you have any questions (702) 998-3700.

The easiest way to provide trust services is to partner with an independent advisor-friendly corporate trustee in a tax-favorable jurisdiction that focuses exclusively on the administration of trusts. IconTrust, LLC (ICON) can fill that role. ICON is a Nevada Chartered advisor-friendly trust company. Advisor-Friendly means the trust company does not manage investments, draft trusts, or prepare tax returns. ICON’s role is to administer trusts in coordination with a client’s existing professional team. If ICON has investment discretion within a trust document, ICON will typically delegate that role to the client’s existing financial advisor.

The advisor must feel secure with the advisor-friendly trust company, its business model, and its procedures. The advisor must feel confident with the trust company’s brand and the customer service provided by its trust officers. At the end of the day, the advisor’s client is a client of the trust company, and the advisor is hired by the trust company to provide investment management. The trust company must do nothing to jeopardize the relationship between the advisor and the advisor’s client, only enhance it.

Financial advisors who want to broaden their client relationships to offer trust services under an extension of their existing brand may be interested in a private label trust services relationship (PLT). A PLT relationship is established with a comprehensive PLT Services Agreement between the financial advisor and an existing trust company. The financial advisor will receive a brand name for their private label trust services, e.g., PWM Trust Services, and branded client statements. The financial advisor will typically pay a one-time setup fee to establish the PLT relationship and a revenue share can be created with the trust company. The trust company, for example, ICON, retains all fiduciary liability and must sign off on all marketing materials for the financial advisor’s private label. A separate phone number is issued by ICON in the name of your private label brand. A representative of the PLT partner and a representative of the trust company will work together to provide ongoing training and marketing support.

The private label is a middle ground between referring to an advisor-friendly trust company and starting your own trust company.

Some financial advisors are not comfortable with giving up a level of control in a partnership with an independent advisor-friendly trust company and would rather go through the rigorous process of starting their own trust company. These firms must be comfortable with setting aside capital, hiring trust officers, creating the corporate and compliance framework, and assuming 100% of the fiduciary liability.

A trust company can be chartered by a particular State or by the Office of the Comptroller of the Currency (OCC). Whether chartered by a particular state or by the OCC, a trust company would typically be subject to certain capital requirements, require a fidelity bond and/or E&O insurance, along with complying with BSA/AML standards like most other financial institutions. For example, in Nevada, the capital requirement is $1M, and a physical office in Nevada staffed with a trust officer is required. Further, a chartered trust company in Nevada will typically need another $500k - $1M in operating capital.

Most “family office” trust companies are state-chartered and are established under one of the top four trust jurisdictions (NV, SD, DE, AK). These states are typically business-friendly, have no state personal or corporate income tax, possess the top assets protection statutes, and permit the use of Dynasty Trusts to last several generations.

The barrier to entry in the four top jurisdictions is very similar and an advisor must make sure they want to assume the financial risk and liability associated with starting a trust company. Profitability can be elusive, possibly taking several years.

Financial advisors have been successfully implementing each of these options in providing trust services to their clients. One choice is not better than the others. The advisor must decide how important their brand is when working with their trust clients and how much control they want over the trustee relationship. Partnering with an advisor-friendly trust company, starting a trust company, or creating a private label arrangement all solidify client relationships across multiple generations.

If you have any questions about a referral or private label trust relationship with ICON, please email info@icontrustnv.com or call 702-998-3700.

A Nevada Asset Protection Trust is a trust you create for your own benefit to protect your assets from potential creditors during your lifetime.

The assets transferred to the trust should be considered a rainy-day fund and should not be assets you need to live off regularly. You should make sure this trust is set up when there is no known, threatening, or pending creditors. If you have a creditor looming and transfer assets to an asset protection trust, the transfer will most likely be considered fraudulent. Finally, you should not overfund the Nevada Asset Protection Trust. A good guideline would be to not place more than 50% of your assets into a Nevada Asset Protection Trust. If you do, an argument can be made that you are insolvent.

Under Nevada’s statutes, you may retain certain control and powers when it comes to the asset protection trust. You can be your own investment trustee to determine what the trust buys and sells without disqualifying the trust’s asset protection. You should not, however, be your own distribution trustee. The distribution trustee should be a third-party, not related to or subordinate to you, or a trust company. If you need funds in the trust, you would request a distribution from the distribution trustee. The asset protection comes from the fact that the distribution trustee must approve the distribution - you cannot.

You do not have to live in Nevada to set up an asset protection trust. The majority of our clients do not live in Nevada but set up a Nevada asset protection trust to benefit from Nevada’s laws. For an out-of-state client one of the easiest ways to qualify a trust under Nevada law is to have one trustee or co-trustee be a Nevada resident or Nevada trust company. A quick list of unique features of Nevada’s laws are below:

In our experience, the average cost to have a qualified estate planning attorney draft an asset protection trust is somewhere between $5,000 - $10,000. The cost of having a trust company serve as trustee can be anywhere between $3,000 - $5,000 per year.

I am betting you want to know if they definitively work. The answer is "Maybe". There has not been a lot of case law one way or the other. This should give you some confirmation of their effectiveness. If you are still skeptical, estate planning attorneys have created a hybrid domestic asset protection trust. In the hybrid trust, you may be able to indirectly access trust assets through your spouse, and it’s a third-party trust which offers definitively more protection than a self-settled trust.

If you have any other questions, please email us at info@icontrustnv.com or call 702-998-3700.

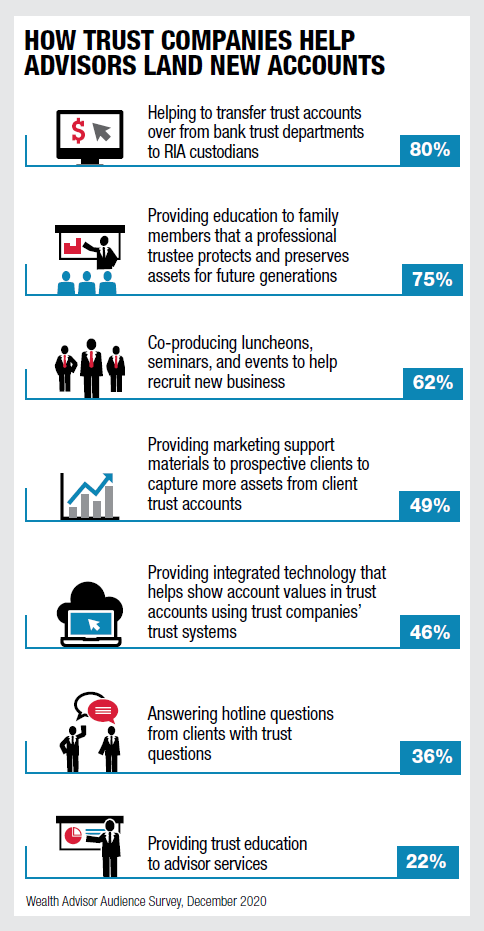

The America’s Most Advisor Friendly Trust Companies guide was released this week by The Wealth Advisor, a leading voice in the financial services industry. This guide details 21 of the best non-custodial, non-management trust companies in the industry. IconTrust is the newest company on the list.

To view our profile or download the full guide click below.

The trust companies on this list partner with advisors instead of competing for assets under management. They realize that investment management is best provided by the client's trusted financial advisor and trust administration is best provided by an independent corporate trustee. This is in stark contrast to the traditional trust companies of the past that handle both sides; trust administration and investment management. Many clients prefer the separation of duties, flat trustee fees, and the greater flexibility of an advisor-friendly trust company.

"A trust account is an investment account with instructions. You handle the investment account, we handle the instructions."

The average consumer is smarter than ever before and knows that investment management can sometimes be a bit of a commodity. They are reminded of computer-based platforms that can supposedly match market returns for a fraction of the price of a financial advisor. This is why managing trust accounts is such a differentiator in the marketplace. Providing trust services goes beyond asset management and into deep conversations about legacy planning and family dynamics that can solidify advisor relationships for many generations. Trust assets are sticky and working with an advisor-friendly trust company is a financial advisor’s glue to the next generation.

With a new political administration and a potential of a decrease in the estate tax exemption, wealthy families will need estate tax planning advice in 2021 and beyond. For advisors, there has never been a more opportune time to partner with a law firm and an advisor-friendly trust company to offer estate planning services. Advisors who are proactive in providing advice in this potential new tax environment are poised to attract many new wealthy families to their business.

IconTrust was founded in 2020 and is the newest trust company to the list of America’s Most Advisor Friendly Trust Companies. Years of experience in an outdated and archaic trust industry prompted us to create a new model for advisors and their clients. We think charging trustee fees based on assets under administration is outdated. Our flat trustee fees for all types of trusts are easier for advisors to promote and for clients to understand.

We feel our flat fee schedule for all trust services is a true differentiator in the marketplace. We built IconTrust with simple procedures and simplified fees that everyone can understand. We believe our model will set a new standard for how a modern trust company should operate and provide services to advisors and their clients.

To learn more about Icon's Benefits for Financial Advisors contact us at 702-998-3700 or email info@icontrustnv.com.

A trust settlement checklist is a must-have if you have been named as successor trustee on a trust. After the death of an individual, their estate plan needs to be administered. This process is called post-mortem administration and is a series of tasks performed by a fiduciary named in the estate planning documents. The fiduciary of a trust is called a successor trustee.

Serving as the successor trustee of a trust is not a role to be taken lightly. Administration can be an arduous and time-intensive project even for a professional trustee, let alone an individual trustee who may not be familiar with the fiduciary duties and liabilities they are undertaking. If you have been named as successor trustee on a trust, the following checklist may serve as a guide of some of the duties you may perform in settling the trust and carrying out the wishes of the decedent.

If you have any questions about the above trust settlement checklist, please email info@icontrustnv.com or call 702-998-3700.

A corporate trustee is a bank or independent trust company that is licensed to act as trustee of a trust.

The primary function of a trustee is to administer trust assets according to the grantor’s wishes while considering the interests of the beneficiaries of the trust.

In a traditional trustee arrangement, one trustee wears all three hats. The trustee is responsible for the investments, distributions, and administration of the trust. Thankfully, over the last twenty-five years, many states have amended their laws to allow for the splitting of trustee duties, commonly referred to as a directed trust arrangement. This arrangement allows for the bifurcation or trifurcation of trustee duties giving trust grantors, beneficiaries, and their professional advisors more control over a client’s estate plan. Grantors can now decide which hats they want their trustee(s) to wear and what powers they retain. The grantor can select one sole trustee with full powers, or multiple trustees to wear different hats and retain only certain powers.

Irrevocable Trusts

If you are setting up an irrevocable trust while you are alive, you will need a trustee to act today. Some of the reasons you might set up an irrevocable trust are for asset protection, gifting, estate tax planning, income tax planning, charitable planning, opportunity shifting, etc. You will need to separate yourself from the assets and having a trustee in a top trust jurisdiction can be to your benefit for state income tax savings and asset protection.

Revocable Trusts

There are many factors to consider if you have a revocable living trust and are looking for a successor trustee to take over in the event you become incapacitated or pass away. Please look at the following chart to determine whether a family member or a corporate trustee makes the most sense within your estate plan.

| Individual | Corporate Trustee | Advantage | |

| Experience | Do they have experience serving as a trustee? Do they know the responsibility & liability of serving? Do they want to serve? | Has Trust Officers trained in trust administration with expertise in record-keeping, tax and trust law. | Corporate Trustee |

| Time / Resources | Do they have the time required to administer a trust? Do they have the appropriate resources? | Has a full-time dedicated staff and a network of estate planning professionals. | Corporate Trustee |

| Cost | Has the discretion to charge a fee, usually drafted into the trust document, or determined by state statute. | Should have a published fee schedule on their website. Usually more expensive than an individual trustee. | Individual Trustee |

| Knowledge of the Family | May have more intimate knowledge of the grantor, his or her wishes, and the beneficiaries | May have less intimate knowledge of the grantor, his or her wishes, and the beneficiaries. | Individual Trustee |

| Impartiality / Objectivity | Biased. It is very difficult for individuals to not show biases during trust administration. Can they make difficult decisions without emotion, strictly based on the trust provisions? | Unbiased. They can only do what the trust document tells them to do. They are not affected by emotion and have the appropriate tools to make difficult decisions. | Corporate Trustee |

| Location for state income taxes | Do they live in a state with a state income tax or a creditor friendly jurisdiction? | Does the corporate trustee reside in a favorable jurisdiction like Nevada for tax and creditor protection? | Corporate Trustee |

| Continuity | What is their age? | Corporate trustees continue in perpetuity. | Corporate Trustee |

| Removal process | Will they resign if asked by the beneficiaries? | Run a business and will typically resign if asked by the beneficiaries. | Even |

| Regulated / Insured | Not regulated. | Financially stable and carry insurance to protect the beneficiaries. | Corporate Trustee |

For more information please give us a call at 702-998-3700 or email info@icontrustnv.com