To really understand the benefits of directed trusts, you must first understand the differences between a traditional "delegated" trust and a more modern "directed" trust.

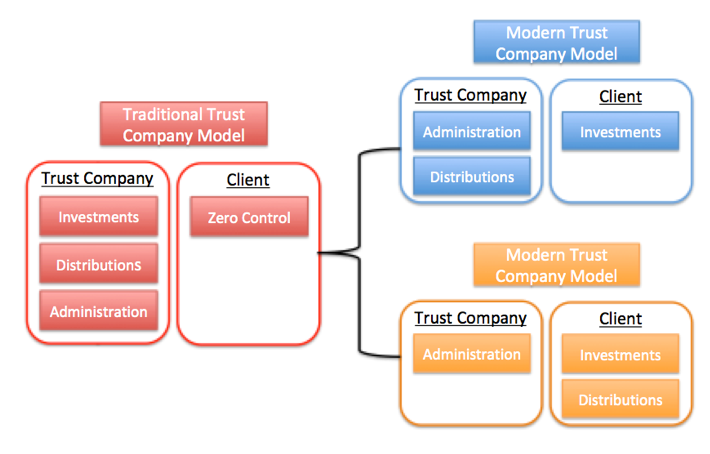

In a traditional trust arrangement, a corporate trustee is responsible for making decisions on investments, distributions, and for the administration of trust assets. All three functions are typically handled in-house. We call this the bundled approach. A trust company may either offer investment management services or delegate investment management to a third party. The trustee still has the ultimate fiduciary responsibility to monitor and oversee the investments and typically will charge a fee based on the market value of the underlying assets, subject to fluctuations in the stock market.

In a directed trust arrangement, the trust document allows for the splitting of trustee duties into multiple roles: an Investment Trustee with the sole discretion to make investment decisions on behalf of the trust, a Distribution Trustee with powers to make or authorize distributions from the trust, and an Administrative Trustee responsible for maintaining books and records and signing tax returns and other documents in an administrative capacity. We call this the unbundled approach. Clients see the value of a corporate trustee for situs, tax, and administration but would prefer to work with their existing professional team of advisors for the investments and perhaps the distribution functions of their trust. A directed trust gives trust grantors, beneficiaries, and their professional advisors more control over a client’s estate plan. Once a cutting-edge planning technique, directed trusts are now the preferred trust structure of the wealthy.

In a directed trust arrangement, the investment management responsibility is removed from the corporate trustee, thus removing the investment liability. This is important because a trustee’s liability for the underlying investments is typically a major factor in determining trustee fees. If the corporate trustee has no investment liability then its fee should be less. Many directed trustees charge a flat fee instead of an asset-based fee to administer a directed trust because of this reduced overall liability.

Given the option, most clients would like to determine what their trust can buy, sell, and hold. They want an advisor they know and trust to manage their investments. They see the value in a corporate trustee administering their trust, but they want the expertise of their trusted financial professionals along the way. Wealthy clients also have nontraditional assets such as, closely-held businesses, family limited partnerships, LLCs, private equity interests, etc., which may not fit under a corporate trustee’s investment parameters. A directed trust allows clients to preserve, protect, and grow these unique assets that are core components to their family’s financial success.

“The task is not to control the wind, but to direct the movements of the ship so that it stays on course.”

Wealthy clients are used to controlling their destiny. They are the captain of their ship, and they like it that way. In estate planning, clients must be willing to give up some level of control, but to the extent they can retain as much as possible, they would prefer it that way. We have discussed giving the client or their trusted financial professional investment discretion in their trust, but some clients also want to give a family member or committee the power to authorize distributions from the trust. They feel this would give more peace of mind and protection for their beneficiaries with fewer restrictions. In a directed trust, they can do just that. The distribution trustee or distribution committee will be able to direct the corporate trustee on when to make a distribution from the trust to a beneficiary.

Nevada has one of the most powerful directed trust statutes in the country. NRS 163.

If you have any questions about directed trusts, please email info@icontrustnv.com or call 702-998-3700.

The following key benefits of Nevada law have made Nevada the top trust jurisdiction in the United States. You do not have to live in Nevada to take advantage of Nevada's favorable trust and tax laws.

Nevada does not tax individuals or trusts at the state level.

Commonly referred to as the rule against perpetuities, a Nevada trust may last 365 years. A trust lasting 365 years, combined with no state income taxes levied at the death of each generation, can create substantial compounding growth over multiple generations.

Allows for the splitting of trustee duties into multiple roles: An Investment Trustee or Investment Advisor, with the sole discretion to make investment decisions on behalf of the trust, an Independent trustee or Distribution Trustee with powers to make distributions from the trust, and an Administrative Trustee responsible for maintaining the books and records of the trust.

Legally termed Nevada Self-Settled Spendthrift Trusts

A grantor may create an irrevocable trust in Nevada for their own benefit. The grantor is the creator of the trust as well as a permissible beneficiary. NAPTs are established to protect a portion of the grantor’s assets during the grantor’s lifetime. Nevada is one of only 19 states that allow self-settled trusts and is consistently ranked as the top self-settled trust state for the following reasons:

f you have any questions about the key benefits of Nevada law, please email info@icontrustnv.com or call 702-998-3700.

There is little doubt Nevada has taken over as the top trust jurisdiction in the United States. For years the estate planning community has looked to states like Delaware and Alaska for their favorable tax and asset protection laws. Not anymore. The top estate planners in the country are increasingly using Nevada as their preferred out of state trust jurisdiction for high net worth clients and their families.

Nevada enacted its domestic asset protection statute in 1999. A Nevada asset protection trust (NAPT) is an irrevocable trust in which the creator of the trust is also a permissible beneficiary. Two years after the creator transfers a portion of their assets to the trust, those assets should be protected from all creditor claims. A Nevada asset protection trust is a vehicle to protect assets from creditor claims which are becoming more prevalent in our highly litigious society.

Nevada is unique with one of the shortest statutes of limitations, with most domestic asset protection trust states having a four-year statute. Nevada is also one of only two states that have no exception creditors. These are creditors that can pierce the trust irrespective of a state's statute. Nevada has none. Sixteen of the nineteen domestic asset protection trust states have exception creditors, including a divorcing spouse for child support and alimony, in addition to other potential creditors.

Nevada does not have a state income tax. Therefore, a trust sitused in Nevada will be responsible for filing a federal income tax return, but there is no corresponding Nevada tax or filing. Investable assets held inside a Nevada trust can compound substantially without having to pay state income taxes. To learn more about which states are most tax-friendly for the wealthy, read the recent USA Today article posted in January 2020: https://www.usatoday.com/story/money/2020/01/29/the-most-tax-friendly-states-for-the-rich/41060485/

A directed trust allows for the separation of a trustee's roles among multiple parties. The old traditional trust had one trustee responsible for the investment, distribution, and administration of a trust. A handful of states have enacted directed trust statutes which allow the investment and distribution functions to be handled by a family member, friend, or other trusted advisor while leaving the administrative functions to a corporate trustee.

The unbundling of trustee services gives trust grantors, beneficiaries, and their professional advisors more control over a client’s estate plan. Clients prefer the separation of duties, flat trustee fees, and the greater flexibility of a directed trust arrangement.

Decanting is the act of pouring assets from an old trust to a new trust with more favorable terms. For years estate planners struggled with the simple fact that irrevocable trusts were irrevocable and could not be changed. Nevada's decanting statute allows for the modification of an irrevocable trust to address changes in trust law and dynamics within families that could not have been predicted. Some of the most commons reasons to decant are to change drafting errors, trustee provisions, distribution standards, and governing law.

The length of time a trust can last is dependent on the state’s "Rule Against Perpetuities." In 2005, Nevada's laws were amended to allow a trust to last for 365 years. This means a trust in Nevada can last for 365 years without the trust assets being subjected to an estate tax levied at each generation. The current estate tax exemption for 2020 is $11.58M for an individual and $23.16M for a married couple. Any amount over these thresholds is subject to an estate tax of 40%. These current estate tax exemption amounts push Dynasty Trusts down to #5 on our list of why Nevada is the #1 state for trusts. One thing we do know about estate taxes is they are subject to change. If the estate tax exemptions are lowered through sunset of the current law, or through a change in administration, the Dynasty Trust would move up in the ranking of why Nevada is the #1 state for trusts.

To learn more contact us at 702-998-3700 or email info@icontrustnv.com.